Trends Report 2018 – Future Shock is Now

As content creators, producers, or broadcasters, how do we remain realistic, critical, vigilant, and confident that we will continue to have a viable role to play in the globalized content market?

Download this reportIntroduction

→ This Trends Report is also available in Spanish: Informe de tendencias 2018 – El choque del presente.

The relentless march of technology, artificial intelligence, and robotics have certainly left their mark on 2017. For some, the conclusions are alarming, but others are optimistic. Regardless of the outlook, the fundamental question is the same: How does the human set itself apart from the machine? Is technology our friend or foe? Should we fear its consequences?

This legitimate concern is even more important for the creative and cultural industries. Is it possible to remain creative and innovative in a world of similarities powered by algorithms? How do we stay competitive in a media sector dominated by technological titans? How do we adapt our business models in a space where automation is clearly taking over? In a generalized context of mistrust, what can the content creation and distribution sectors do in the months ahead?

This report published by the Canada Media Fund outlines four major trends that have originated from the convergence and interaction of various phenomena developing at great speed; we must be particularly attentive to them in 2018.

The report presents a selection of main indicators of how the Canadian industry is evolving, an overview of the four main trends and 10 attached appendices explaining the phenomena associated with each trend. Each appendix includes an “Attention Barometer” to help Canadian content producers assess how attentive they should be to the phenomena within the scope of their professional activities.

RESEARCHED AND WRITTEN BY :

- Catalina Briceño, Director, Industry and Market Trends

- Pierre Tanguay, Analyst, Industry and Market Trends

- Sabrina Dubé-Morneau Analyst, Industry and Market Trends

- Gaëlle Engelberts, Editorial Coordinator, Industry and Market Trends

Dashboard

All data refer to the Canadian market, unless otherwise indicated.

*** ***

*** ***

*** ***

*** ***

*** ***

*** ***

*** ***

*** ***

***

1. Finding a Counterbalance to Online Giants

As already mentioned in our Trends Reports, the digital revolution has changed business models and given rise to new global giants. While some giants have acquired a stronghold in a specific industry (Netflix for streaming, Steam for video games), others dominate in a wide range of sectors from equipment and software to social media and electronic commerce, and content production and distribution. Google, Apple, Facebook, Amazon, and Microsoft, best known under their acronyms GAFA or GAFAM, are well known in western regions. Other giants are surfacing elsewhere around the world. For instance, Baidu, Alibaba, Tencent, and Xiaomi (BATX) are common in China. The effects are the same as western regions: hyper-concentration and oligopoly.

The open and borderless internet has given way to a few digital ecosystems controlled by powerful private businesses some say are similar to “Virtual States” (see Splinternets appendix). These businesses control online infrastructures (including cloud computing), browsers, apps stores, operating systems, and search and referral engines. They set technical standards and pricing. In addition, they funnel investments into research and development, especially in artificial intelligence, used extensively to exploit the wealth of data they gather on users.

Does this mean that everyone, users and media professionals alike, is doomed and subject to the whims of today’s digital titans? We think not.

We have seen that algorithms have their limits. This year, fake news has multiplied, dodgy content has slipped into once-protected environments (including a major setback to YouTube Kids), and advertisers have been up in arms about their brands being connected to objectionable content on Google’s ad networks.

Nobody, however, can deny the benefits of super-platforms. They capture the attention of most worldwide users, disseminate content catalogues globally, and provide publishers with feasible monetization avenues, attracting the lion’s share of advertising dollars.

2017 could be considered our year of awareness, for we noticed the digital giants’ strangleholds and many flaws. 2018 will be a year of enlightenment, where content creators, producers, and broadcasters must learn to better negotiate their presence on and collaboration with the super-platforms while making better use of the technologies that define our digital landscape.

Reaction has been organized at the user and government level for some time now. Examples include the €2.42 billion fine levied against Google for abusing its dominant position, the €13 billion claim against Apple for unpaid taxes in Europe, measures taken in various countries to control the major platforms even more (among others, Google v. Equustek Solutions decision by the Supreme Court of Canada in June 2017 requiring Google to delete information from its search engine), or the growing number of US elected officials claiming that the activities of the online giants should be reviewed in light of antitrust laws (like what was done with AT&T, IBM, and Microsoft in the past). In short, GAFA is being scrutinized by authorities around the world in what many are calling a real ‘techlash.’

Business is also taking steps: we see major players in television and film giants such as Disney, HBO, and Fox are regaining control of their catalogues and removing their content from Netflix and Amazon Prime Video. Others are forming or strengthening alliances to better compete against the digital behemoths: European Media Alliance; South Korea’s Kocowa platform; and advertising partnerships such as Nonio in Portugal, Gravity Alliance in France, Emetriq in Germany, and OpenAP in the United States.

Emerging technologies promoting decentralization are also becoming popular, as is observed with blockchain, where many media and content creation applications are being assessed and tested (see Blockchain appendix). However, many observers are skeptical. Blockchain technology is closely linked to cryptocurrencies like Bitcoin and Ether, which are very volatile and far from being universally accepted. And while the technology has been in development for several years, it has generated few tangible results to date.

Despite these uncertainties, investors remain confident: 2017 investments in the technology reached US$1 billion and the blockchain market itself could be worth trillions in a few years according to some analysts. In terms of the cultural industries, blockchain technology can play a role in optimizing the use of digital cultural products (security, traceability, integrity of data), while cutting out the middleman.

Appendices associated with this trend:

2. Appropriating Technology for Creative Purposes

Where some see threats, others see opportunities to foster creativity. The ubiquity of social media and the rapid rise of technologies, such as artificial intelligence, are being ingeniously explored by storytellers. Consequently, the grammar of storytelling is evolving rapidly and becoming multi-format. From Twitter stories written in installments of 140 characters or less1 to hijacking game creation engines for developing narratives for television or virtual reality, there are numerous examples of new technologies playing a role in storytelling.

Social Storytelling

Social media are not a new phenomenon; they have always been testing grounds for creators. American Matt Richtel coined the term twiller—a combination of Twitter and thriller. In 2008, he wrote It Should Be Snowing, his first twiller composed of 220 tweets, spread out over a six-month period. As of 2013, fifteensecond serialized fiction episodes appeared on Instagram, the year the platform started to share videos.

In the last few months, social media experiences have increased, giving way to more sophisticated storytelling. One of the keys to understanding this trend is found in the proliferating use of chatbots, offering a possibility for stories to be directly told in messaging apps, blurring the line between conversation and fiction (see Chatbots appendix).

A good example of the judicious use of social media in storytelling lies in the Norwegian teen series SKAM. The series did not have a fixed broadcast schedule; instead, it rolled out short online clips in real time when the action takes place. To keep the plot going after the episodes have aired, the characters published content in real time on Facebook and Instagram, encouraging fans to follow the story and directly interact with characters from their social media news feeds. SKAM was a huge success in Norway. The third season averaged 600,000 viewers per episode in a country of just five million people. Broadcasters around the world have bought adaptation rights for the series, but Facebook has put its hand on an English-language adaptation for its Watch platform.

Technology as an ally

To boost rapid introduction of new technologies, platforms are providing features and application program interfaces (APIs) to explore new genres. Apple made ARKit available, making it easy to develop augmented reality applications. In October 2017, ARKit was the most downloaded iOS app from the App Store. Then in November, Amazon rolled out SUMERIAN, an app used to develop 3D environments for virtual and augmented reality (see Augmented Reality appendix).

Many innovative projects get off the ground when connections are made between disciplines that are rarely complementary. Here is one striking example: TFO (Télévision française de l’Ontario) is using the popular and free Unreal Engine to create stunningly realistic virtual sets at much lower cost. The technology opens the door to new possibilities for television virtual sets and tremendous creative freedom for screenwriters.

Artificial intelligence can be of use, too. Researchers at the Massachusetts Institute of Technology (MIT) recently developed machine-learning models that can “watch” video clips and establish their emotional arc. Machines can identify the story’s strong points, aiding creators to determine and increase the impact of their work on audiences.

Data-based creation

Technology developers and big digital platforms help publishers gain a better understanding of their audiences through the use of Big Data, encouraging content creation that is better aligned with the consumers’ interests.

The key benefit of making intelligent use of connected technologies and digital distribution is accumulating usage data that can, in turn, influence content creation and increase the creators’ and producers’ agility. Data can help producers and creators better understand their audiences, ultimately optimizing content and marketing—sometimes in real time.

The clearest example of this quasi-symbiotic relationship between creation and data is illustrated with streamers (see Streamers appendix). They are masters in the art of collecting and analyzing data, and reacting to their fans during live broadcasts.

Appendices associated with this trend:

3. Audio’s Revenge

According to many observers, the online experience is changing because of the quick adoption of mobile use. With voice recognition and voice activation technologies (see Voice Recognition & Activation appendix) and the growing popularity of virtual assistants such as Siri, Alexa, and Google, more and more users are moving away from keyboard-and-text-based experiences and turning to voice and audio experiences. Unlike chatbots that respond to text commands, voice robots interpret and execute voice commands.

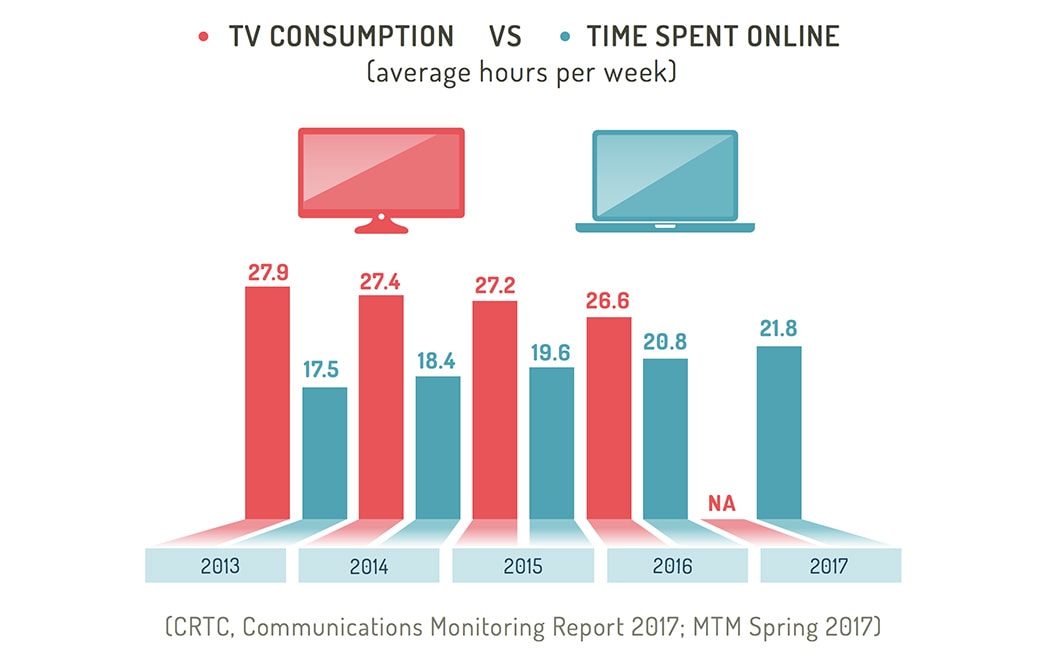

Statistics show that we have reached a plateau for time spent in front of our screens. According to Zenith, media consumption in North America increased by only 1.8% in 2017 and declined slightly on a global scale. So far, time dedicated to online activities has added to time used to consume traditional media in many regions, including Canada. As we reach a point of saturation, online and traditional media now compete to capture users’ attention. Media consumption can now increase only if users are not confined to keyboards and screens; instead, they must be given options to consume and interact with content while doing something else.

Listening to audio online—especially podcasting (see Podcasting appendix)— has grown in popularity in the past two years. According to Edison Research, in the United States, listening to audio content online increased from 12 hours and 8 minutes per week on average in 2016 to 14 hours and 39 minutes in 2017. In Canada, the Media Technology Monitor reports that the average listening time increased from about five hours in 2015 to more than six hours in 2017.

The increase in online audio consumption is stimulated by the continued popularity of listening to traditional radio—an activity more popular than some online activities. As surprising as it may seem, people still spend more time with traditional radio than with social media.

Audio is becoming increasingly important in the virtual and augmented reality sectors, too. In 360° immersive experiences, sound is key to maintaining visual continuity and sensory immersion: when users turn away and change their field of vision, the characters and objects around them continue to exist because of sound. Audio developments in the virtual and augmented reality sphere have been truly spectacular. Many leading content publishers, such as the British Broadcasting Corporation (BBC), have already put the development of binaural sound at the top of their list (see Binaural Listening appendix).

Appendices associated with this trend:

4. Business Models: Advertising’s About-Face

The advertising business model remains central to the digital content economy. But is it under threat? Some analyses point to that direction further to recent events such as the continued rise of ad-blocking technology (see Ad Blocking appendix), the growing mistrust toward programmatic advertising (see Programmatic appendix), and the ongoing difficulty of accurately measuring advertising impact and return on investment across all media platforms.

Several analyses from firms such as eMarketer, Zenith, and GroupM are downgrading their growth forecasts in several advertising markets, including Canada’s. Deloitte goes so far as to identify an adalergic user type we’re seeing more and more of online. To counter this trend, advertisers need to find strategies to circumvent ad blockers. This can be done by promoting advertisements on mobile devices and social media.

Other firms, such as IAB, are less alarmist. There is a consensus, however, that the online advertising model needs to be reviewed to improve transparency, demonstrate more efficiency, and better meet users’ needs and expectations. A handful of giants increasingly control the online advertising market more and more these days; this is true in Canada and elsewhere around the world, as already stated in the first chapter. “The top ten internet companies now account for 87% of all revenue, up from 77% in 2009,” the Canadian Media Concentration Research Project stated, adding, “Google and Facebook dominate the internet advertising market, with nearly three-quarters of the market between them in 2016—up from a little under two-thirds a year earlier.”

Content industries have observed that they must find revenue alternatives considering the increased rejection of online advertising. Microdonation is an avenue that is now being explored by bloggers and news media outlets such as The Guardian.

The subscription model is yet another alternative. Although the impact of online advertising continues to grow, according to Deloitte, per-user revenue has gone into freefall. As researcher Leora Kornfeld explains in an article published on our CMF Trends blog, advertising is no longer sufficient to meet needs. Many content creators are diversifying their income sources, in part turning toward subscription models.

We think that money in advertising will always be available. After all, this is a strong market, costing US$535 billion on a world scale ($11 to $13 billion in Canada according to analyses). The question is, how will this money be spent in the next few years? An increasing proportion of ad spending could bypass the content industry’s ad inventories altogether, with advertisers choosing to invest in new advertising formats and experiences. Branded entertainment will likely continue to evolve as experiential and influence marketing constantly grow.

Appendices associated with this trend:

Conclusion

Today’s trends point to a tomorrow where robotics, algorithms, and artificial intelligence will play an ever-greater role in shaping our world. Additionally, the technosphere is moving toward an economic rationale dominated by the digital ecosystems of a small number of powerful stakeholders. We must prepare for more artificial intelligence, more control, and more consolidation among the greatest stakeholders. At the same time, there will be more interest in alternative offerings, new story formats, and original and diversified niches that take advantage of new technologies and digital uses. Also expect more potential safeguards in advertising, news, and regulation, at least in areas where stakeholders are working to counterbalance internet giants.

The question is not so much whether you play for the optimists or pessimists. Rather, the question to ask at this report’s conclusion is:

As content creators, producers, or broadcasters, how do we remain realistic, critical, vigilant, and confident that we will continue to have a viable role to play in the globalized content market?

We have seen that the content market is moving towards a supernova of inventiveness because creativity will always be the best interface between human and machine. It’s all about actively participating in the evolving digital landscape and using our smarts to take our rightful place in the process.

Catalina Briceño, Director, Industry and Market Trends, Canada Media Fund