Closer, Wider, Faster

The Canada Media Fund's 2020 trends report in the audiovisual industry.

Download this report

Introduction

Could audiovisual content bring us closer and interactive experiences unite us? Granted, that’s not what immediately comes to mind when one thinks about our devices, platforms and digital services. Many would argue, in fact, that they have isolated and divided us like no other force before them. Nevermind that — a strong case for tech-enabled togetherness is emerging.

A technology’s functionalities are not limited to the device’s technical properties, but also — and especially, I would say — to the social and cultural relationships that their users develop among themselves and with objects (Vyas, Chisalita and Van der Veer, 2006).

Young people under the age of 25 make up 40% of the world population. They want to be together, and they convene online via mobile devices. Be it Twitch, Fortnite or TikTok, these platforms are now venues where youths gather to consume content, create their own and share it with each other. These platforms are today’s malls, enabling youths to shop, play, attend concerts, watch movies and — importantly — do all that with their friends.

Content distribution platforms are therefore engaged in a fierce competition to draw audiences, young and old, eager to access cultural products online. The battle between video streaming platforms is certainly one of the most visible aspects of this clash of titans. These new giants are competing for talent, acquiring storied content and developing original intellectual property, spending billions in the process. As the issue of the day consists of offering more content while keeping subscription costs affordable, new opportunities arise for creators.

At any rate, content consumption is not going to decrease, and mobile networks will need to be updated to fit the needs and habits of an increasingly on-the-go clientele. That is where 5G comes into play.

With data transmission speeds 10 to 20 times faster than what is currently possible, 5G could completely transform our media consumption patterns. Many claim that augmented and virtual reality will finally reach their full potential. We are told that 5G will enable us to transpose human interactions in digital environments, in real-time, better than ever before.

Whatever happens, finding the quickest and easiest way to connect with one another remains the name of the game for consumers.

We find ourselves at the outstart of a new decade, needing connections (Closer), facing an ever-growing content offer (Wider), and using technologies that keep honing and accelerating its distribution (Faster).

Catherine Mathys

Director, Industry and Market Trends

This report offers a few figures related to the development of the Canadian industry and a trend analysis divided into four chapters: technology and innovation, media consumption, evolving business models, and markets and competition.

Dashboards

Click to enlarge any figure below. You can consult our sources by clicking on the hyperlinks in the PDF version of Closer, Wider, Faster available via the button at the top of this page.

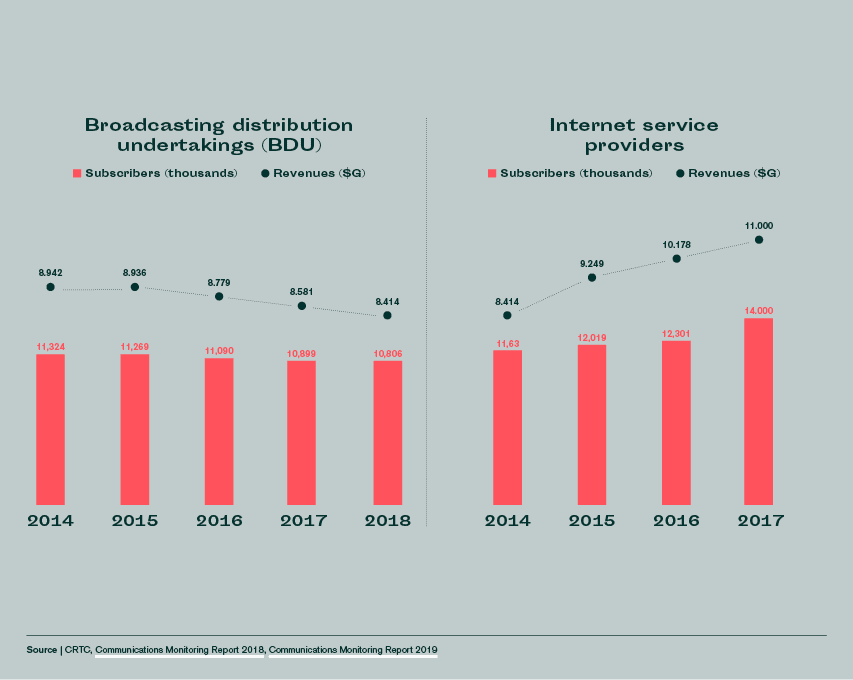

Media consumption in Canada

The Canadian media market

1 - Technology & Innovation: Screen-Based Industries in the 5G Era

The “G” in 4G and 5G stands for “generation,” whereas the number represents the technology’s evolution. Each generation of wireless network brings forth its share of changes in speed, technology, capacity, latency, and infrastructure. 4G, which has been the standard in Canada since 2010, will gradually give way to 5G, which should begin rolling out in 2020.

The “G” in 4G and 5G stands for “generation,” whereas the number represents the technology’s evolution. Each generation of wireless network brings forth its share of changes in speed, technology, capacity, latency, and infrastructure. 4G, which has been the standard in Canada since 2010, will gradually give way to 5G, which should begin rolling out in 2020.

However, 5G isn’t just an evolution of previous generations of wireless communication infrastructure: it’s a technology that will enable real-time data transmission. Simply put, the jump from 4G to 5G will be more substantial than the transition from 3G to 4G has been.

In this chapter, we will take a thorough look at the technological breakthroughs 5G will usher in and ponder their potential impacts on the production and distribution of media content.

1.1 - What Will 5G Change?

4G networks have enabled access to broadband services via mobile devices, with the user’s experience being practically on par with that of a wired connection. That being said, 4G technology have difficulties combining speed, reliability, and energy efficiency. Current 4G/LTE networks can, for example, ensure high-quality video transmission — but only to a limited number of simultaneous users.

A greater number of simultaneous connections

5G promises to tackle this issue by supporting a greater number of simultaneous connections, which will allow smartphones, wearables, sensors, self-driving vehicles, robots, and other connected devices to share bandwidth without encumbering the signal. IMT-2020 (the designation for the norms for 5G networks, devices, and services issued by the International Telecommunication Union) predicts a connection density of a million devices per square kilometre, compared with approximately 2,000 devices for the same area on 4G networks.

Ultra-fast download speeds

5G networks should offer download speeds of 20 Gbps — about 20 times that of 4G networks. A feature-length film on an optimal 5G network would then take about a second to download.

Taking everyday downloading conditions into account, the average reliable speed per user will more likely oscillate around 100 Mbps — significantly less than optimal 5G, but still ten times faster than a 4G network’s capacity.

Very low latency

Latency refers to data transmission delay. The standard for 5G networks anticipates ultra reliable, low-latency communications (URLLC) of under a millisecond. That is far lower than the 50-millisecond latency standard of 4G networks.

URLLC norms will enable us to better connect and interact in real-time. For instance, augmented and virtual reality experiences will be improved as 5G allows for real-time human interactions in digital environments. Such technological advancements could be highly beneficial to virtual reality-based training and education programs, for example.

1.2 - Worldwide 5G Deployment

If 5G is generally perceived as the next breakthrough in mobile communications, it will not change our lives overnight. A Canalys report suggests that 5G’s pivotal year might be 2023.

The global deployment of 5G networks to date has been gradual: 13 commercial networks have launched in 2018 and 40 more in 2019. Ambitious forecasts predict 45 percent of the world’s population would have access to 5G by 2024. The GSM Association estimates that 5G could contribute US$2.2 trillion to the global economy over the next 15 years.

The race to 5G

Several countries are racing to deploy 5G networks. The stakes are high due to the breakthroughs and capacities associated with the technology, which could grant the frontrunners a competitive edge. In its Global 5G Landscape Report, Business Insider Intelligence pins the United States, South Korea and China as the three current 5G leaders.

Once the 5G rollout fully underway, subscriptions in Asia and North America could tally up to more than one billion in three years’ time. In contrast, the same markets accounted for 417 million 4G subscriptions, five years after 4G networks had launched.

The situation in Canada

A report by Accenture Strategy for the Canadian Wireless Telecommunications Association (CWTA) states that 5G networks’ economic impact would contribute $40 billion to Canada’s GDP by 2026. 250,000 year-round jobs would be created over the same time frame.

In April of 2019, a handful of Canadian companies purchased 600 MHz spectrum licences, which operators are hoping to use to rollout 5G networks. These companies are Bragg, Freedom, Iris, Rogers, SaskTel, TBayTel, Telus, Vidéotron and Xplorenet. (Bell did not purchase any licenses at this auction because it already possesses other low-frequency spectrums.)

The Canadian Internet Registration Authority (CIRA)’s latest Internet Factbook indicates that 86 percent of Canadians have broadband internet access. The majority of those who do not live in rural and remote communities that sit out of reach of our current infrastructure. Wireless 5G could therefore be an efficient way to improve connectivity in these regions, at a cost 40 percent below that of fibre-optic internet.

5G connectivity in remote areas: the BBC’s example

The BBC is testing live radio broadcasts over 5G mobile networks in Stronsay, Orkney, as part of the wider 5G RuralFirst initiative. Several other tests will explore the potential of 5G for rural businesses and communities across the U.K. “Using a modified version of the new BBC Sounds app and a broadcast- ready smartphone, those taking part in the BBC trial will be among the first to receive live radio broadcasts over 5G.”

1.3 - What 5G Means for the Screen-Based Industries

What business opportunities is 5G opening up for content producers and distributors?

Large companies are interested in the technology’s potential and added value for the media and entertainment industries. In the United States, for example, Disney’s StudioLab has already partnered with Verizon to explore the opportunities ushered in by 5G.

In 2019, Walt Disney Studios’ Chief Technology Officer, Jamie Voris, told Variety: “We see 5G changing everything about how media is produced and consumed.”

Among other Canadian 5G initiatives, TELUS has partnered with Montreal-based non-profit organization Zù. The partnership aims to put 5G to the test in sectors such as augmented reality and 3D holograms, mobile gaming, immersive storytelling, live volumetric performances, and 4K streaming.

Toward more reliable live broadcasting

Field production and broadcasting often requires large teams to set up audio and video equipment on-site. Production teams must be able to rely on a stable connection. This can be achieved on 3G and 4G networks. However, a connection can easily become unstable, since the broadcast goes through a public network. 5G networks will fix this issue through network slicing. This will allow operators to allocate portions of their networks to specific use cases or groups to significantly improve reliability.

5G-enabled live production: the Verizon Media Studio in Los Angeles

The studio is equipped with a full-blown 5G node, which enables experimentation with ultra-fast, low-latency wireless data transfers. “One area of focus will be to evaluate 5G’s role in making productions more nimble, and possibly replace the satellite truck still commonly used for TV coverage with a much smaller Set-up,” explained Zeda Stone, head of Verizon Media’s immersive content unit.

Exploiting virtual and augmented reality to their full potential

Many experts believe that 5G will allow augmented and virtual reality to reach their full potential. Most remote and mobile AR/VR experiences being data-intensive, delays and signal interruptions currently hamper user comfort and overall experience. 5G features will make those a thing of the past and lead to a wide array of new services and applications such as immersive movies, video games, live events, learning platforms and more.

Furthermore, cloud-based processing will enable VR/AR content to be streamed from a server rather than executed on a device. This will be less demanding to a VR headset or a phone’s processor, consuming less battery energy in turn.

Reaching mobile users with ease

4G has greatly improved access to audiovisual content for a wide variety of devices, such as smartphones, tablets, smartwatches, etc. However, the quantity and quality of content continue to increase, requiring more bandwidth and processing power.

What’s missing in content distribution is a cheap and effective way to reach mobile users with live, linear content. Germany’s 5G Today project, launched in 2017, began experimenting with ways to distribute content to millions of 5G devices in real time in 2019. “I am delighted that today we can launch the world’s first large-scale test network for 5G broadcasting,” said Ulrich Wilhelm, director general of Bayerischer Rundfunk and chairman of German public broadcaster association ARD. “We must design our future digital communications infrastructure in such a way that everyone can continue to benefit from the diversity of media content.”

Cloud gaming

Estimates unveiled during Openwave Mobility’s Mobile Video Industry Council Livecast show that cloud gaming account for 25 to 50 percent of 5G data traffic by 2022.

5G connectivity will enable players to stream video games without having to download content on their devices. Simply put, they will have access to computer- and console quality gaming, without having to splurge on hardware.

Remotely accessing immersive environments will allow a multitude of players across the planet to interact live in a virtual world. This is why 5G seems essential to real-time gaming, for example, which requires very low latency, a lot of bandwidth, great reliability and access for a multitude of simultaneous users.

> Head over to section 3 for a detailed look at cloud gaming

2 - Consumption Habits: Where the Kids Hang Out

It may look like kids spend an awful lot of time in their rooms, on their screens. But don’t be fooled. Instead of meeting at the mall or the park, they convene on platforms like Fortnite and YouTube, where they socialize and meet other kids. Younger generations have always been early adopters of new technology, and their taste for social platforms is stronger than ever.

In this chapter, we take a look at three 21st-century ‘digital social spaces.’ You will see that in environments such as esports platforms, TikTok, and the upcoming digital Metaverse creative content plays a key role.

2.1 - Generation Alpha: The Children Who Will Shape the Future

‘Alphas’ are born between 2010 and 2025, meaning that a lot of them are not yet walking the Earth as you read this line.

We owe the label to Mark McCrindle, a social science researcher who considers that Alphas will form “the most formally educated generation ever, the most technology supplied generation ever, and globally the wealthiest generation ever.” Without much surprise, technology is a key factor that characterizes this demographic group: Alphas will never experience a world without connected screens or social media, access to on-demand entertainment is completely normal to them and most of their digital experiences will be shaped by artificial intelligence.

For the time being, it is difficult to imagine what will differentiate this generation once it has reached adulthood.

> Download Closer, Wider, Faster‘s PDF version for more data on Canada’s Alpha generation and their media preferences (p.24)

2.2 - Esports: The New Major Leagues, and the New Hockey Night in Canada

“Gaming is not only compelling entertainment, but also a forum where friendships are created and maintained.”

– Gaming 360, Hub Entertainment Research, October 2019

Stadiums filled to capacity. Tournaments with tens of millions of online viewers. Cyberathletes earning seven-figure salaries. While the electronic sports (esports) trend already has mass appeal in Asia, its spread is dizzying and the phenomenon may very well be widespread in North America sooner than later.

In a nutshell, esports is the competitive branch of multiplayer gaming. It is to video games what the NHL, NFL and NBA are to hockey, football and basketball. Although esports is far from being anything new, it has made significant progress in 2019, thanks in large part to the Fortnite phenomenon.

Contrary to popular belief, esports attracts people of all ages, young and old alike. However, young people are a major factor in its spectacular growth.

Media, brands and advertisers alike have become aware of the potential of this 21st century spectator sport. In Canada, both Bell and Rogers have begun broadcasting esports, and RDS now features an electronic sports section on its website. Even though Canada’s ranking in the sector remains modest (Canada ranks 26th out of 41 countries polled by GlobalWebIndex for esports viewing by people aged 16–24, well behind the top-ranked Asia-Pacific region), current trends suggest that the phenomenon will continue to grow over the next few years.

Once again, it is young people who are responsible for the most significant advancements. In both Canada and the U.S., esports is making its way into schools. Extracurricular activities, leagues, tournaments and esports-study programs are popping up in high schools. There are even university scholarships for the most promising cyberathletes. And Canada is not to be underestimated when it comes to cyberathletes. Out of the 20 teams in the Overwatch League, a professional esports league dedicated to the video game Overwatch, two are from Canada: the Toronto Defiant and the Vancouver Titans. Last year, seventeen-year-old Canadian cyberathlete Hayden Krueger nabbed third place at the Fortnite World Cup, earning him a US$1.2 million prize.

What games will the pros of tomorrow play? What gaming worlds will attract the crowds and awaken the passion of the fans, in the same way the Calgary Flames, the Toronto Raptors or the Montreal Canadiens do? Michaël Daudignon, founder of Motivment, maintains that “the massive esports game that appeals to everyone does not yet exist.” Talented creators be warned: game on.

> Download Closer, Wider, Faster‘s PDF version for more data on the global esports landscape (p.28)

2.3 TikTok: The Cultural Lab of Today's Youth, Social Media-Style

“The influencer is playing a central role in our culture, and it’s not new. They’ve always been socialites, people of influence, the Paris World’s Fair. Whatever mecca that people go to for culture is where they go to for culture, and in this moment it’s TikTok.”

– Music producer Adam Friedman, as told to Jia Tolentino in “How TikTok Holds Our Attention,” The New Yorker, September 2019

TikTok is without a doubt THE video social network of the moment. Launched in 2016 by industry powerhouse ByteDance in China (where it’s known as Douyin), and in 2017 internationally, it has grown exponentially, especially among teens.

TikTok took over for both Vine and Musica.ly, two predecessors that were very popular with youth. Vine, a six-second micro-video social network owned by Twitter, shut down in 2017, never quite catching on outside the U.S. Musica.ly, on the other hand, was such a success on a global scale that this lip sync social app, created in Shanghai and devoured by kids, was purchased by ByteDance in 2017 and merged with TikTok in 2018. Today, TikTok is a serious competitor to the likes of Facebook, Instagram and even YouTube among the younger generation.

TikTok Explained

“TikTok is an app for making and sharing short videos. The videos are tall, not square, like on Snapchat or Instagram’s stories, but you navigate through videos by scrolling up and down, like a feed, not by tapping or swiping side to side.

Video creators have all sorts of tools at their disposal: filters as on Snapchat […]; the ability to search for sounds to score your video. Users are also strongly encouraged to engage with other users, through ‘response’ videos or by means of ‘duets’ — users can duplicate videos and add themselves alongside. […]

It’s easy to make a video on TikTok, not just because of the tools it gives users, but because of extensive reasons and prompts it provides for you. You can select from an enormous range of sounds, from popular song clips to short moments from TV shows, YouTube videos or other TikToks. You can join a dare-like challenge, or participate in a dance meme, or make a joke. Or you can make fun of all of these things.” – John Herrman, “How TikTok Is Rewriting the World,” The New York Times, March 2019

Could the infatuation with TikTok be no more than a passing fad, as was the case with Vine before it? Many observers think so. And TikTok is no stranger to the ethical and legal problems faced by many other platforms. In the U.S., the U.K., India and Indonesia, its personal data collection and censorship practices are coming under fire, as well as the way it deals with inappropriate content for children.

In any case, TikTok is the perfect example of a trend that has experienced nothing but growth over the years: technology is increasingly social, creating spaces where culture can be fashioned, shared and appropriated, especially for young users. Much like YouTube, TikTok communities generate their own influencers (Alberta’s Ben De Almeida, for example) and their own celebrities. Some, such as writer/performer/rapper Lil Nas X, have become global superstars. Toronto journalist and essayist Calum Marsh, observing the very subtle ways TikTokers engage with films, even wonders whether there aren’t some future professional filmmakers in the lot.

Several media giants have caught on to TikTok’s marketing potential. Record labels are partnering with TikTok content agencies, such as Flighthouse, to promote their artists. NBC, The Washington Post and Teen Vogue are experimenting with the app to promote their brands. As has often been the case in recent years, however, the most significant progress has been made in China. Douyin, TikTok’s sister app, already supports e-commerce, features mini-games and even mini-dramas such as First Times Actually, which has 1.2 million followers.

If TikTok itself doesn’t survive, the TikTok model, already emulated by the likes of Instagram and other American apps such as Firework, will keep influencing the evolution of future social networks.

2.4 - The Digital Metaverse: A One-Stop Experience Shop

“Fortnite’s most significant achievement may be the role it has come to play in the lives of millions. For these players, Fortnite has become a daily social square – a digital mall or virtual afterschool meetup that spans neighborhoods, cities, countries and continents. […] Examples abound of kids, adults and families simply hanging out or catching up on Fortnite while they play.”

– Matthew Ball, “Fortnite Is the Future, but Probably Not for the Reasons You Think,” REDEF, February 2019

With its quarter-billion (mostly young) players, Epic Games’ Fortnite has grown into a bona fide cultural phenomenon in the past few years.

Much like its rival Roblox, Fortnite is part game, part social network, and part amusement park. We play it, watch it, create content in it and make new friends along the way. Players can even attend live concerts in the virtual presence of millions of other audience members. Digital entrepreneur Timmu Tõke says: “It’s a place. Roblox and Fortnite are true virtual worlds. More like physical places to hang out than traditional games.”

Just like TikTok, these platforms are gradually expanding to offer new content to their communities and, above all, new ways to interact with that content. Fortnite has incorporated several popular brands into its universe: NFL skin tie-ins, characters from the Marvel and John Wick worlds and even a Weezer-themed island, where players can listen to the Californian band’s songs. Fortnite also added voice chat thanks to the acquisition of Houseparty, a chat app for teens.

Facebook is set to experiment with virtual worlds in 2020. The American juggernaut promises to deliver a massive, immersive VR universe with Facebook Horizon, on Oculus Quest and Rift, where visitors will even be able to watch films.

“Starting with a bustling town square where people will meet and mingle, the Horizon experience then expands to an interconnected world where people can explore new places, play games, build communities, and even create their own new experiences.”

– Facebook, September 2019

According to several entrepreneurs and futurologists, virtual worlds such as Fortnite and Horizon are a glimpse not into the future of gaming, virtual reality or social media, but of actual computing platforms and interfaces. They are the first signs of a new digital paradigm, the Metaverse, which will replace smartphones and the internet as we know them today. Whether and when this vision becomes reality remains to be seen.

> Download Closer, Wider, Faster‘s PDF version for more data on Fortnite and Roblox (p.33)

Until then, the current trend is obvious. For hundreds of millions of people, and youth in particular, platforms like Twitch, TikTok, Fortnite and Roblox aren’t just about things to look at on screens. They’re actual places to go to and spend time in, places where you hang out with friends, where you watch and make stuff. Tech and content have never been more social.

What is the Metaverse?

Entrepreneur, investor and former head of strategy at Amazon Studios Matthew Ball explains: “The term ‘Metaverse’ […] describes a collective virtual shared space that’s created by the convergence of virtually enhanced physical reality and persistent virtual space. In its fullest form, the Metaverse experience would span most, if not all virtual words, be foundational to real-world AR experiences and interactions, and would serve as an equivalent ‘digital’ reality where all ‘physical’ humans would simultaneously co-exist. It is an evolution of the Internet. More commonly, the Metaverse is understood to resemble the world described by Ernest Cline’s ‘Ready Player One’ (brought to film by Steven Spielberg in 2018). […]

[Epic Games CEO Tim] Sweeney speaks of the Metaverse in terms of its capabilities to connect humans in new ways. Mark Zuckerberg has often said the same, which was why he acquired Oculus: ‘Strategically we want to start building the next major computing platform that will come after mobile. There are not many things that are candidates to be the next major computing platform… [Oculus is a] long-term bet on the future of computing…. Immersive virtual and augmented reality will become a part of people’s everyday life.'” – REDEF, February 2019

3 - Business Models: Diversification Brings About Change

As they continue to expand their footprint, digital giants like Google, Apple and Spotify are out to conquer new content territories, disrupting the business models of incumbents. How will those models adjust and evolve? Here’s a look into two sectors that are coveted by digital juggernauts: gaming and podcasting.

As they continue to expand their footprint, digital giants like Google, Apple and Spotify are out to conquer new content territories, disrupting the business models of incumbents. How will those models adjust and evolve? Here’s a look into two sectors that are coveted by digital juggernauts: gaming and podcasting.

3.1 - Gaming: A Race Toward the Cloud

Access, as opposed to ownership, is gradually gaining followers in the gaming industry, much like the music, film and television industries before it. Will playing a video game soon be as easy as listening to a song on Spotify or watching a video on YouTube? That’s the experience cloud gaming promises to deliver.

2020: The dawn of cloud gaming

In 2019, more than 2.5 billion gamers spent approximately US$152.1 billion on video games. With US$68.5 billion in sales, mobile gaming represents the lion’s share of the industry. A GlobalWebIndex study conducted in 45 countries in the second quarter of 2019 reveals that 71.5 percent of internet users aged 16 to 64 use smartphones to play video games, meaning there’s already a large number of gamers willing to pay for mobile content.

Concurrently, mobile devices’ operating systems are constantly improving, allowing game developers to offer better gaming experiences and to release titles that can compete with PCs and consoles.

All this is paving the way for multiplatform cloud gaming’s bright future. Zion Market Research predicts a 27 percent annual growth for the sector over the next six years, with expected sales of $6.9 billion in 2026.

What is cloud gaming?

The term refers to several practices, but essentially the concept is the same as with any on-demand music or video service: the game is stored and run on a remote server, then streamed to a user’s device.

For example, imagine a gamer who decides to try her favourite studio’s newest release while waiting for the bus. She pulls out her phone and launches into a new adventure in under two minutes. Once home, she puts down her phone, turns her smart TV on and picks up where she left off. Two hours later, the game reveals itself to be a drag. Not to worry: her streaming service membership includes access to the studio’s entire catalogue, and 100 hours of gameplay per month. In a previous era, she would have had to spend a few hundred — if not thousand — dollars on a gaming computer or console, another eighty-odd dollars on the game, and would have waited an hour or two for it to download and install. All that to lose interest two hours in.

However, all of this is still out of reach for the time being.

There are nevertheless two technological challenges to overcome before cloud gaming can really take off: network performance and data usage.

The first is crucial to gaming: no one wants to suffer the frustration of lagging due to a bad connection, especially in the case of massively multiplayer online games (MMOG), such as Fortnite or League of Legends, where a fast, stable connection is fundamental.

The second is self-evident: unlike many major markets, unlimited data plans are not the norm in Canada. Let’s take a look at Google Stadia, for example, the web giant’s cloud gaming platform, unveiled in 2019. According to PC Gamer, even the recommended minimum streaming requirements for a mobile game would consume 4.5 GB of data per hour, making it easy to exceed your cell phone plan’s data limit.

There is a solution on the horizon: 5G, which was examined in the first chapter. The new generation of mobile networks will provide gamers with infinitely faster and more stable connections, ideal for cloud gaming, among other things. Whether the arrival of 5G will spell the end for limited data cell plans remains to be seen.

The industry’s key players are making their moves

Many web and video game giants have announced their foray into cloud gaming over the past year, during which progress was made for both subscription- based downloadable game libraries and “native” cloud gaming.

The arrival of tech giants in the cloud gaming industry may trigger a race, but it is difficult to predict how quickly gamers will embrace it. According to David Cole, CEO of research firm DFC Intelligence, cloud gaming is nowhere near posing a threat to the conventional console business because consistent business models have yet to be established. However, Ubisoft co-founder and CEO Yves Guillemot believes that consoles only have one more generation left in them before cloud gaming becomes the industry standard.

What will the impact on business models be?

The transition to the cloud comes with its share of benefits and challenges for intellectual property owners in the gaming industry. A publisher with its own subscription-based cloud gaming platform can count on recurring revenue, reducing its need to rely on the crucial holiday season. It will nevertheless have to be technologically — and financially — competitive with the tech giants. And their cloud gaming services will be able to rely on an international network of state-of-the-art servers.

Others could establish themselves as content providers for the more successful cloud gaming platforms. However, Google Stadia’s example sheds a light on a potential complication: Google opened its own game development studio for Stadia in the fall of 2019 to diminish its reliance on for third-party developers.

Will we witness the arrival of a “Netflix of gaming,” a games aggregator that would eliminate the need to subscribe to many platforms at once? If so, how would revenue sharing work?

It’s easy to see that we’re dealing with a wide range of possibilities, as well as a considerable number of unanswered questions, when looking at the impact cloud gaming will have on the evolution of the gaming industry’s business models. The stakes are particularly high in Canada, where the gaming industry is thriving.

3.2 - Podcasting: Spotify Is Shaking Up the Industry

Even though podcasting still is a relatively small piece of the media industry taken as a whole, you would be hard-pressed to find another medium generating a comparable amount of enthusiasm.

While it is clear that there are plenty of listeners and that ad revenue will continue to increase, the sector is faced with two obstacles: it must convince its audience to pay for content, and it must strengthen its ability to attract advertising dollars.

The race to paid subscriptions: Spotify is making waves

With 248 million monthly users, including 113 million subscribers paying for Spotify Premium as of Q3 2019, Spotify is pulling the rug from under podcasting incumbents hoping to further monetize their audiences through subscriptions.

Spotify Premium’s 113 million subscribers can now use the service to listen to podcasts without any ads (other than host-read ads that are part of an episode per se).Furthermore, since acquiring Gimlet Media, Spotify can boast the catalogue and exclusive content of one of podcasting’s most popular content publishers. To top it off, the streaming platform is ordering shows from third-party producers, such as Michelle and Barack Obama. The company’s strategy seems to be paying off: Spotify’s podcast audience almost doubled between January and August of 2019.

Spotify is therefore well positioned to grab a large share of the increasing revenue generated from podcast subscriptions, partly thanks to its consolidated audio offer—the platform notoriously offers its users some 50 million songs, positioning it as a one-stop shop for audio content. We see similar integrated models in Canada, with services such as CBC Listen, Ohdio and Qub Radio each offering their own assortment of audio content. Of those, however, none monetize listenership via subscriptions, and none host content other than their own.

Spotify is not the only major player to be positioning itself more and more aggressively in the podcast space. Apple, Amazon and Luminary are all doubling down on their efforts and investments.

These platforms will likely try to one-up one another in the hopes of attracting big names and producing exclusive content that will increase the number of paid subscriptions. The risk in this model is the fragmentation of a previously more open distribution ecosystem.

The business model for podcast creators and publishers will have to adapt. Will they become content providers for audio streaming platforms?

The race for advertising dollars: Programmatic advertising and improved measurability

The podcast industry generates most of its revenue from advertising, at least for the time being, but podcasting’s ad market is not nearly as developed as its video or digital display counterparts. Rates are still based on the number of downloads instead of the number of active listeners, and ads are still widely sold in the traditional manner. Programmatic ad placement represented only 1.3 percent of the podcast industry’s advertising revenue in 2018.

Again, it’s safe to say that Spotify will help move things along.

The service already allows advertisers to target its free-tier listeners by podcast category and even runs a marketplace that gives companies and ad agencies the opportunity to purchase audio advertising time. In March 2019, programmatic advertising already represented 20 percent of Spotify’s revenue. Even though the platform is in the early stages of programmatic advertising in podcasting, Julie Clarke, Spotify’s global head of automation revenue, confirms that the company is exploring ways to reinvent its advertising experience as the sector transitions towards programmatic.

With regard to measuring ad performance in podcasting, there still remain giant steps to be taken in order to go from the number of downloads to something much more granular. We may have to wait for the new podcasting giants to reach their cruising altitude. “We’ll most likely see a lot of companies specialized in podcast metrics and analytics be swallowed by Spotify, Apple and other services,” according to Nicholas Quah, founder of Hot Pod. “Things will be quiet for a year or two, but once the market settles down, another round of mergers and acquisitions will take place.”

4 - Markets & Competition: Bundling 2.0

Brace yourself for more choice in streaming services in the next year. A great deal of new direct-to-consumer platforms is entering the digital content market, some of them very big. Content producers stand to benefit, but will consumers begin to feel overwhelmed? For many in the media industries, it’s time to rethink—and rebundle — the online content experience.

Brace yourself for more choice in streaming services in the next year. A great deal of new direct-to-consumer platforms is entering the digital content market, some of them very big. Content producers stand to benefit, but will consumers begin to feel overwhelmed? For many in the media industries, it’s time to rethink—and rebundle — the online content experience.

4.1 - Let the Streaming Games Begin!

Friends, The Office, the movies and shows from the Marvel and Star Wars universes… Until now, Netflix subscribers in Canada could watch these hit series on the popular American streaming platform. But that will change before long.

In the near future, many of these popular titles will be offered by new subscription video on-demand (SVOD) services launched by big competitors, notably Disney, Apple and the media conglomerates owned by telecom giants AT&T (WarnerMedia) and Comcast (NBCUniversal).

According to many observers, the “streaming wars” look like they’re going to be more relentless than ever. The competition in the video-on-demand space is already fierce. There are hundreds of subscription-based streaming services, most of which are small or medium-sized and cater to niche audiences. In the U.S., over 300 platforms are already available. In Canada, around 50 services will be available to consumers this year, including Canadian services such as Crave, Club Illico, Gem, Tou.tv Extra, APTN lumi and OUTtv. However, these platforms do not have the resources of multinationals like Netflix and Amazon.

This is not the case for the new American giants entering the streaming arena in 2019 and 2020. Disney, AT&T, Comcast and Apple all have the capital, brands and content catalogues necessary to compete with Netflix and Amazon.

While content spending is soaring (competition for top talent, sharp rise of investments in original content as well as acquisitions), subscription prices remain low, due not only to competition but to consumers’ growing price sensitivity. Netflix lost 100,000 subscriptions in the second quarter of 2019 in the U.S., its first drop in almost a decade, and did not reach its new subscriber target the following quarter. In Canada, a slight market share decrease is forecast for Netflix by 2023, while Canadian streaming service Crave is gaining ground.

The hunt for good old-fashioned sitcoms

The most memorable sitcoms of the nineties and the 2000s have lost neither their appeal nor their market value. Online streaming services are snatching them up, hundreds of millions of dollars at a time, proving that the competition is influencing the cost of streaming rights:

- US$425 million for Friends

- US$500 million for Seinfeld

- US$500 million for The Office

- US$1.5 billion (according to sources) for The Big Bang Theory and Two and a Half Man

Spend more on content, charge less to consumers: the stakes are high for small and medium-sized platforms that can’t rely on tens of millions of subscribers or income derived from other activities, such as ecommerce (Amazon), hardware sales (Apple), tourism (Disney) or telecom services (AT&T, Comcast). Content producers, on the other hand, may benefit from the arrival of new players: more potential buyers, more available funding.

Among these new buyers is Quibi, the mobile, premium short-form content platform, set to launch in 2020 with Jeffrey Katzenberg and Meg Whitman, respectively Hollywood and Silicon Valley icons, at the helm. With funding in the billions of dollars, Quibi is interested in Canadian talent and has already signed development deals with Bell Media and Look Mom! Productions. Other Canadian producers could see their order books fill up in the coming years.

4.2 - Out with the Old, in with the... Old?

A myriad of content options is already available to internet users, and even more are yet to come.

Platform launch announcements have been on the rise for months: BET+, Pluto TV and Pluto TV Latino from another American giant, Viacom; a new documentary platform from the BBC and Discovery; Salto from France Télévisions, TF1 and M6; etc. In Canada, TV broadcaster APTN (Aboriginal Peoples Television Network) celebrated its 20th anniversary last year and launched lumi, a video-on-demand platform dedicated to Indigenous content. “Today, the choice is up to the viewer,” states Monika Ille, APTN’s CEO. That’s why a lot of companies are betting on direct-to-consumer services. The important thing is to establish direct relationships with customers.

Will this explosion of streaming services confuse or, worse, exhaust consumers? Early signs already pointed towards saturation in the U.S. at the beginning of 2019, when Ampere Analysis observed a slowdown in growth in SVOD “stacking” (consumers subscribing to multiple video-on-demand services). Deloitte, United Talent Agency and GlobalWebIndex also sounded the alarm in their 2019 spring and fall reports, citing consumer frustration in the U.S. and the U.K.

“Despite the huge uptake of subscriptions services, consumers still express some dissatisfaction. The biggest frustration is the sheer cost of managing multiple services. Even though some subscriptions are modestly priced, it all adds up. As more services enter the mix, how far will consumers be willing to stretch their wallets to get the content they want? (…) Bundling services together at a discounted price is one potential way of keeping consumers engaged and creating more value.”

– Katie Gilsenan, Is Entertainment Subscription Fatigue Setting In?, GlobalWebIndex, July 2019

It seems that bundles, those packages of channels long offered by traditional pay-TV providers, are reemerging in the digital universe. Often criticized for their prices and lack of flexibility, these bundles are once again on the table, given the dispersal of content on an ever-growing number of competing digital services. Several digital bundles have been offered for some time, whether it’s through web platforms (Hulu+ Live TV, YouTube TV, Amazon Prime Video Channels), media streaming sticks (Roku) or telecom and cable TV providers (Comcast’s Xfinity Flex). Others have recently launched or are under development, in Canada and elsewhere.

The bundling phenomenon is consistent with wider trends affecting all consumer markets online. To gain a competitive edge, online platforms are striving to achieve the widest possible aggregation of product while offering the narrowest possible targeting and personalization to individual consumers. On the latter front, some tech analysts warn that current bundling models may fail to rise to the challenge if they remain too focused on the “big box” approach of traditional pay-TV. Bundling provides more volume, but not necessarily more convenience: the right content on the right screen at the right time.

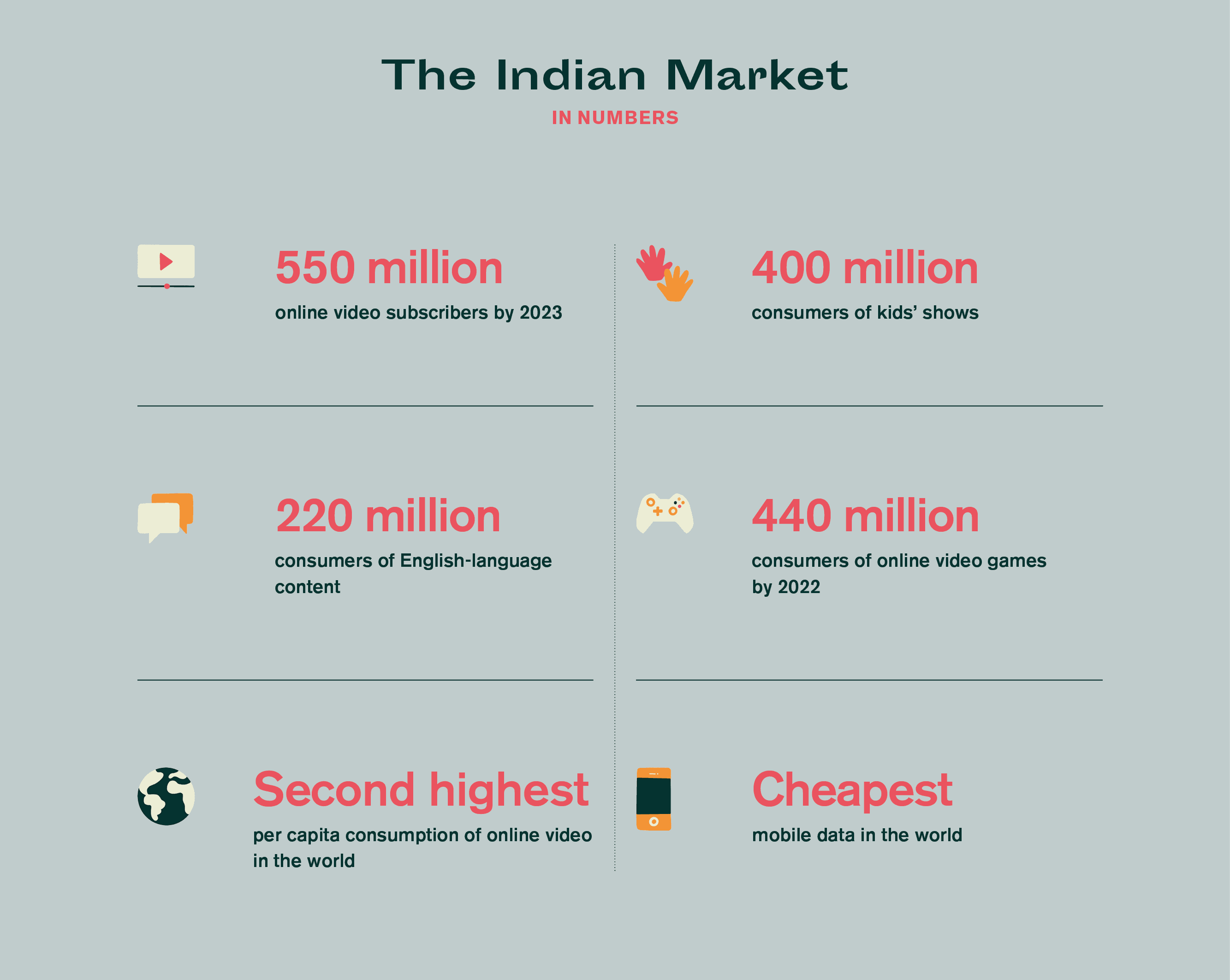

4.3 - India, a Market Worth Keeping an Eye On

Several Canadian businesses have successfully entered the Indian market in the past few years: Essential Media Group, Squeeze Studio Animation, Blue Ant International, Wattpad, QYOU Media, etc.

An audiovisual coproduction treaty with Canada and trade agreements with Ontario and British Columbia have been signed. Zee Entertainment Enterprises, India’s largest private TV broadcaster, even decided to establish a production facility in British Columbia: Zee Studios International, which will produce content for global markets.

Canadian media industries are well positioned to do business in India, and vice versa. In many ways, trends in India and the rest of the world are quite similar, although they seem more pronounced in India. Take a look at the following data and you’ll notice that the major trends of “mobile, affordable and local” are making great strides: overwhelming predominance of mobile video, aggressive pricing (including new and innovative approaches such as sachet pricing and lower-priced mobile-only subscriptions) and, as opposed to Western markets, significant lead of local platforms over foreign services.

The bundling trend is very well set up in India. A recent KPMG study particularly highlights the rapid increase of partnerships between online video platforms, both local and foreign, and the country’s telecom service providers. There’s also a surprising twist: rival content platforms are partnering up. “For example, the KPMG study reports, Zee5 and Alt Balaji have forged a content sharing arrangement to co-create original content in Hindi, which will be available exclusively on both the platforms.”

The Asia-Pacific region is often at the forefront of new trends in terms of technologies and consumption, as mentioned in our 2017 Trends Report. Could the rapid transformation of digital media and telecoms in India be an indicator of what the future has in store for markets in Canada and the rest of the world?

To be continued…

Contributors

This report was written and researched by:

- Catherine Mathys – Director, Industry and Market Trends

- Pierre Tanguay – Manager, Industry Research, Industry and Market Trends

- Maxime Ruel – Editor, CMF Trends, Industry and Market Trends

- Laurianne Desormiers – former Editor, CMF Trends, Industry and Market Trends

- Sabrina Dubé-Morneau – Special Projects Lead, Industry and Market Trends

- Daphnée Brisson-Cardin – Graphic Designer and Illustrator

For questions about this report, contact us: [email protected]